100% committed to saving you time and money.

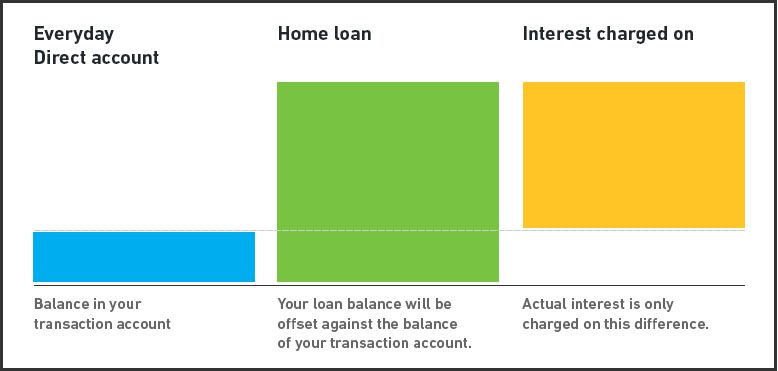

A mortgage Offset facility is an eligible transaction account linked to an eligible home loan account. Instead of being charged interest on the full loan balance, interest is charged on the loan balance minus the balance in the Offset account. Read on to see how an Offset facility works, plus more.

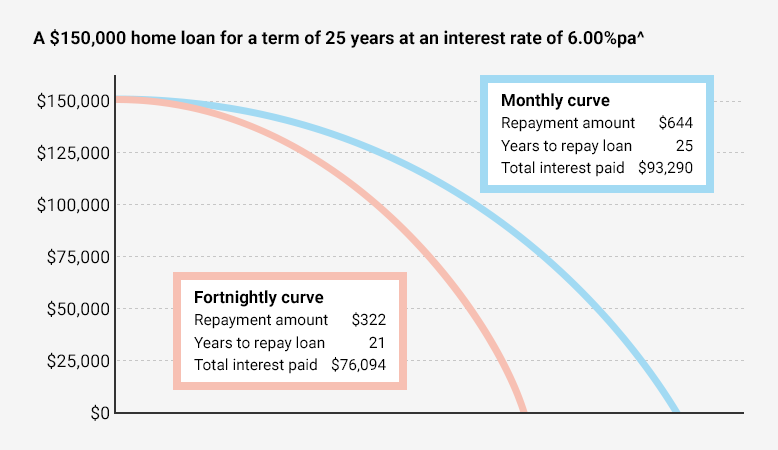

You can further shorten the time it takes you to repay your home loan by making fortnightly home loan repayments, as well as using the 100% mortgage offset facility. Paying fortnightly allows you to make the equivalent of one extra monthly repayment per year. The following scenario gives you an idea of how this works.

When you apply for a home loan with Australian Mutual Bank, you can also apply for the mortgage offset facility. This allows you to link up to 8 Everyday Direct accounts to your home loan. This means that, instead of being charged interest on your full loan balance, interest is charged on your loan balance minus the combined balance of the Everyday Direct accounts linked under the mortgage offset facility.

100% offset is available exclusively through the Your Way Plus Home loan package on:

Please note: Each Your Way Plus home loan can have up to 8 Everyday Direct accounts linked under the mortgage offset facility. Each Everyday Direct account can only be linked to one Your Way Plus home loan at a time.

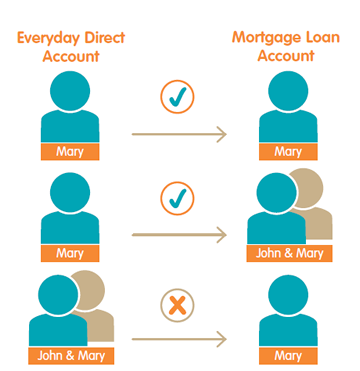

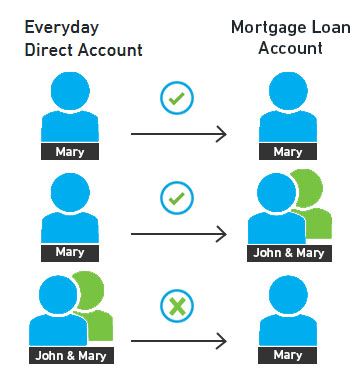

Possible scenarios in which you can attach an Everyday Direct account to a home loan account for Offset purposes:

Possible scenarios that are not permitted for attaching an Everyday Direct account to a home loan account for Offset purposes:

Important information: The Australian Tax Office requires Offset facilities to be set against accounts that are owned by the same person or persons. This means that person A cannot have their home loan offset by a transaction account owned by person B. However, if person A and B own a home loan together, (i.e. the home loan is in joint names) either one may have their individual transaction account linked to their joint home loan.

Here are some examples of how an Offset facility can work for you:

This example assumes that, on one particular day, the following facts apply in relation to a member's accounts:

(a) a home loan account with a debit balance (dr) of $100,000;

(b) a linked Everyday Direct account with a credit balance (cr) of $10,000; and

(c) an interest rate of 6% per annum applying to the home loan.

(d) the Offset percentage is 100%.

The balance of your linked Everyday Direct account ($10,000 cr) is offset against the balance of your home loan account ($100,000 dr).

The result, the Offset balance, is $90,000 dr:

For the purposes of charging interest, the balance of the home loan account loan is split into two portions:

And, in charging interest:

The calculation and the result are as follows:

($10,000 x (6% - (100% x 6%)) + ($100,000 - $10,000) x 6%) ÷ 365

|

Please note: The above is an example only. Interest rates may change at any time and we may change the Offset Percentage at any time upon notice to you.

This example assumes that, on a particular day, the following facts apply in relation to a member’s accounts:

(a) a home loan account with a debit balance (dr) of $7,500;

(b) a linked Everyday Direct account with a credit balance (cr) of $10,000; and

(c) C. an interest rate of 6% per annum applying to the home loan;

(d) the Offset percentage is 100%.

The balance of your linked Everyday Direct account ($10,000 cr) is offset against the balance of your home loan ($7,500 dr). The result, the Offset balance is $2,500 cr.

The interest rate applying to the home loan account balance ($7,500) is reduced by the Offset Percentage which, in this example, is 100% of the home loan rate and the debit balance owing on your home loan is reduced by the equivalent amount from your linked transaction account. No interest is paid by us on the credit balance of the linked transaction account.

Yes, you can have both a redraw facility and an Offset facility.

You can link up to 8 Everyday Direct accounts to one Your Way Plus home loan. Each Everyday Direct account can only be linked to one home loan at a time.

No, there are no restrictions on the loan amount to qualify for the Offset facility.

There is no actual minimum of maximum, however if the offset account balance is zero or in debit no Offset will be calculated for those days. If the Offset account balance is greater than the loan, no Offset benefit will be calculated for the amount that exceeds the loan balance, for the days in the month the Offset balance exceeded the loan balance.

The owner of the Everyday Direct account must be the owner of the mortgage loan, or one of the owners in the case of joint mortgage loans.

Yes, every owner of the Everyday Direct account must be also an owner of the mortgage.

1. Terms and conditions for the mortgage offset facility are set out in our Consumer lending terms and conditions and Conditions of use - Accounts and Access. For more information refer to the FAQ section under Offset facility at www.australianmutual.bank. Conditions of use - Accounts and Access document and Fees and charges brochures are available online or from any of our offices. You should read both of these documents before deciding to open accounts and access facilities issued by Australian Mutual Bank. Any advice provided here does not take into consideration your objectives, financial situation, or needs, which you should consider before acting on any recommendations. For further information call 1800 800 225.

2. Fees and charges and lending criteria apply. Consumer lending terms and conditions available from any of our offices.

Teachers Mutual Bank Limited ABN 30 087 650 459 AFSL/Australian Credit Licence 238981.